Buying your first home in New Zealand is one of the biggest financial decisions you will make. Between government schemes, lending restrictions, deposit requirements and the buying process itself, there is a lot to get your head around before you sign anything.

This guide walks you through every step of the first home buying journey in New Zealand. It covers how much you can borrow, where your deposit can come from, which government support you may qualify for, how lending rules affect your options, and what happens from pre-approval through to settlement day.

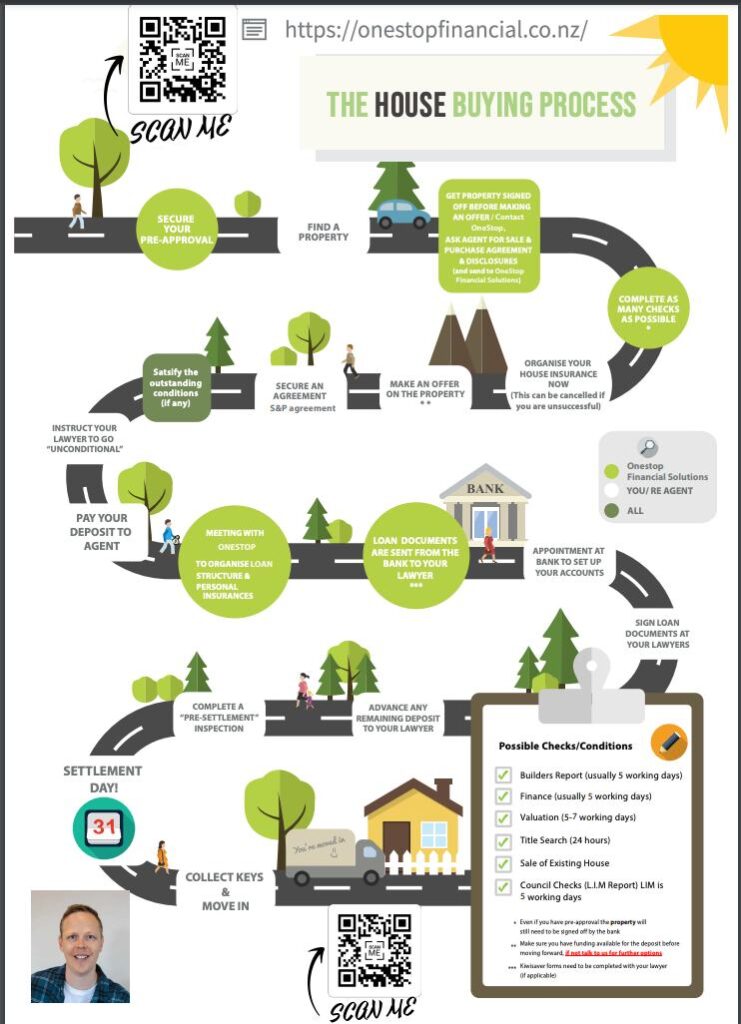

Here is a visual of the process:

How Much Can You Afford as a First Home Buyer?

Before you start looking at properties, you need a clear picture of what you can realistically borrow and repay. Two main rules govern how much a bank will lend you:

- The loan-to-value ratio (LVR), and;

- The debt-to-income ratio (DTI).

Beyond those, banks also stress test your ability to make repayments at a higher interest rate than you will pay on day one.

Work Out Your Borrowing Power

Your borrowing power is determined by your gross (before tax) income, your existing debts, living expenses and the current stress test rate banks apply. Most banks stress test at around 2.5% to 3% above the advertised rate to make sure you can still afford repayments if rates rise.

As a starting point, owner-occupier borrowers are limited to total debt of around six times their gross annual income under the Reserve Bank’s DTI restrictions.

If your household income is $120,000 and you have no other debts, the maximum you could borrow is roughly $720,000. If you have a $10,000 car loan and a credit card with a $5,000 limit, those reduce your borrowing capacity by $15,000 before you even look at a mortgage.

Banks count your credit card limit, not your outstanding balance. If you have a $10,000 credit card limit but owe $0, the full $10,000 still counts against your DTI. Close or reduce unused credit facilities before applying for a home loan. This includes buy now pay later programs like Afterpay.

Budget for the Full Cost of Owning a Home

Your mortgage repayment is not the only cost. You also need to budget for rates, insurance (house and contents), maintenance, body corporate fees if buying a unit or apartment, and utilities. A common rule of thumb is to allow 1% to 2% of the property’s value per year for maintenance and ongoing costs on top of your mortgage.

Standard Deposit Requirements

Most banks in New Zealand require a 20% deposit for owner-occupiers. On a $700,000 home, that means $140,000. However, first home buyers can purchase with less than 20% through several pathways.

| Deposit Size | Who It Applies To | How to Access |

|---|---|---|

| 5% | First home buyers meeting Kainga Ora criteria | Kainga Ora First Home Loan through participating lenders and mortgage brokers |

| 10% | Owner-occupiers via bank or non bank low-deposit products | Apply directly with your bank or through a mortgage broker |

| 20% | Standard requirement for all owner-occupiers | Standard lending, no additional fees or margins |

| 30% | Investors (existing properties) | Required under RBNZ LVR restrictions for investment lending |

Where Your Deposit Can Come From

Banks accept deposits from several sources, but each comes with documentation requirements.

Personal savings: The most straightforward source. Banks want to see consistent saving over time, typically demonstrated through three months of bank statements.

KiwiSaver withdrawal: If you have been a KiwiSaver member for at least three years, you can withdraw your savings (minus $1,000) to put toward your first home. This is covered in detail in the next section.

Gifted deposit: A non-repayable gift from family is accepted by all major banks. You will need a signed gift declaration confirming the money does not need to be repaid, along with evidence of the source of funds. Banks treat gifts differently from loans. If the money needs to be repaid, it counts as debt and reduces your borrowing capacity.

Inheritance or lump sum: Accepted, but you will need to show evidence of where the funds came from.

Sale of assets: Proceeds from selling a vehicle, shares or other assets can count toward your deposit with proof of the transaction.

Banks review your bank statements for the past three months. Unexplained lump sum deposits will be questioned. If family is gifting you money, have them transfer it well before you apply and keep a clear paper trail.

Using KiwiSaver to Buy Your First Home

KiwiSaver is one of the most powerful tools available to first home buyers in New Zealand. If you meet the eligibility criteria, you can withdraw almost your entire balance and put it toward your deposit or purchase price.

Eligibility

To qualify for a KiwiSaver first home withdrawal, you must meet all of the following criteria:

- You have been a member of KiwiSaver (or a complying superannuation fund) for at least three years.

- You have never owned a home or land before, in New Zealand or overseas. Previous homeowners may qualify as a “second-chance buyer” — see below.

- You intend to live in the property you are buying. You cannot use KiwiSaver to buy an investment property.

- You have not made a first home withdrawal before. You can only ever make one.

- You are a New Zealand citizen, permanent resident, or ordinarily resident in New Zealand.

What You Can Withdraw

You can withdraw your personal contributions, employer contributions, government member tax credits and all investment returns. However, at least $1,000 must remain in your account. Any funds transferred from an Australian complying superannuation scheme cannot be withdrawn (though investment returns on those funds can be).

How the Withdrawal Works

Your KiwiSaver provider processes the withdrawal, not Kainga Ora (unless you are a previous homeowner applying as a second-chance buyer). The process works as follows:

- Contact your KiwiSaver provider for a balance estimate. You will need this for your home loan pre-approval.

- Once you have a signed sale and purchase agreement, complete your provider’s first home withdrawal application form.

- The form includes a statutory declaration that must be witnessed by a Justice of the Peace, solicitor or other authorised person.

- Submit the form along with your sale and purchase agreement and a letter of undertaking from your solicitor.

- Once approved, the funds are paid directly into your solicitor’s trust account, either as a deposit (if conditional) or at settlement.

Allow at least 10 to 15 working days for the withdrawal to process. If you are buying at auction, you cannot use KiwiSaver for the auction deposit because you need an unconditional agreement. However, you can use it at settlement. Plan accordingly.

Second-Chance Buyers

If you previously owned a home but no longer do, you may still qualify. Kainga Ora will assess whether you are in a similar financial position to a first home buyer. This assessment considers how long ago you owned property, your current realisable assets and whether those assets exceed 20% of the regional price cap.

Contact Kainga Ora directly at firsthome.withdrawal@kaingaora.govt.nz or call 0800 549 472 to request an assessment.

2026 Update: KiwiSaver Rule Changes for Service Tenancy Workers

From 2026, the Government is amending the KiwiSaver Act to allow workers in service tenancies (such as farmers, rural teachers and defence personnel who live in employer-provided housing) to withdraw their KiwiSaver for a first home purchase without needing to live in the property. First-time farm buyers will also be able to use their KiwiSaver toward purchasing a farm through a commercial entity they majority own, where it will be their principal residence.

Government Support for First Home Buyers

Kainga Ora First Home Loan

The First Home Loan is a government-backed mortgage that allows eligible first home buyers to purchase with as little as a 5% deposit. Kainga Ora underwrites the loan, which means participating lenders can offer financing that would otherwise sit outside their standard lending criteria. This loan is exempt from the Reserve Bank’s LVR restrictions.

Eligibility Criteria

- You must be a New Zealand citizen, permanent resident, or resident visa holder ordinarily resident in New Zealand.

- You must be a first home buyer, or a previous homeowner in a similar financial position to a first home buyer.

- Your before-tax income from the past 12 months must be $95,000 or less (individual without dependants), or $150,000 or less (individual with dependants, or two or more buyers).

- You must have a minimum 5% deposit.

- You must intend to live in the property for at least six months.

No Property Price Caps

Since June 2022, there are no longer property price caps on the First Home Loan. You can purchase any property as long as you meet the income caps and the lender’s own credit criteria.

Lender’s Mortgage Insurance (LMI)

First Home Loan borrowers pay an LMI fee of 1.2% of the loan amount. This can be paid upfront or added to your loan balance. On a $600,000 mortgage, the LMI fee would be $7,200. While this is a cost, a key benefit of the First Home Loan is that most participating lenders offer their standard or special interest rates to First Home Loan borrowers, without the low equity margins that typically apply to low-deposit lending outside the scheme.

Participating Lenders

First Home Loans are available through ASB, Westpac, Kiwibank, Co-operative Bank, SBS Bank, Unity Money and NBS. You apply directly through a participating lender, not through Kainga Ora. A first home buyer mortgage broker can help you identify which lender is the best fit for your situation.

Kainga Whenua Loans

If you want to build or relocate a home on multiple-owned Maori land, you may be eligible for a Kainga Whenua Loan. The loan cap is $500,000, with a 15% deposit required on every dollar borrowed above $200,000. This scheme is separate from the First Home Loan and has its own eligibility criteria.

LVR Restrictions Explained

Loan-to-value ratio (LVR) restrictions are rules set by the Reserve Bank of New Zealand (RBNZ) that limit how much low-deposit lending banks can do. They determine the minimum deposit you need to buy a property.

Current LVR Settings (as at 1 December 2025)

| Borrower Type | Maximum High-LVR Lending (Speed Limit) | Minimum Deposit |

|---|---|---|

| Owner-occupiers | 25% of bank’s new lending can be above 80% LVR | 20% (or less if within the 25% allowance) |

| Investors (existing properties) | 10% of bank’s new lending can be above 70% LVR | 30% |

| New builds | Exempt from LVR restrictions | Set by individual lender |

| Kainga Ora First Home Loan | Exempt from LVR restrictions | 5% |

How LVR Is Calculated

LVR is your loan amount divided by the property value. If you are buying a $700,000 property with a $140,000 deposit, your loan is $560,000. Your LVR is $560,000 ÷ $700,000 = 80%. An LVR of 80% or below means you have a 20% deposit and are not classified as a high-LVR borrower.

What “Speed Limits” Mean for You

The 25% speed limit for owner-occupiers means that banks can allocate up to 25% of their new lending to borrowers with less than a 20% deposit. In practice, most of this allocation goes to first home buyers. Whether you can access a low-deposit loan depends on your bank’s remaining capacity at the time you apply. Working with a mortgage broker gives you visibility across multiple lenders and their current appetite for low-deposit lending.

LVR Exemptions

The following types of lending are exempt from LVR restrictions and do not count against the bank’s speed limit:

- Kainga Ora First Home Loans

- New build purchases (borrower commits early in construction or buys within six months of completion)

- Refinancing where the new loan does not exceed the original loan value

- Bridging finance

- Property remediation (e.g. fixing a leaky home or bringing a rental up to Healthy Homes standards)

DTI Restrictions Explained

Debt-to-income (DTI) restrictions have been in effect since 1 July 2024. They cap how much total debt you can have relative to your gross annual income. DTI restrictions work alongside LVR restrictions. You need to satisfy both to get a standard bank home loan.

Current DTI Thresholds

| Borrower Type | High-DTI Threshold | Speed Limit |

|---|---|---|

| Owner-occupiers | Total debt exceeding 6x gross annual income | 20% of bank’s new lending can be high-DTI |

| Investors | Total debt exceeding 7x gross annual income | 20% of bank’s new lending can be high-DTI |

How DTI Is Calculated

Your DTI ratio is your total debt (including the proposed new mortgage) divided by your total gross annual income. All debts count: existing mortgages, personal loans, car loans, student loans, buy-now-pay-later balances and credit card limits. Income includes salary, wages, self-employment income and in some cases rental income, though banks apply their own treatment to different income types.

The same exemptions apply as LVR, including new builds, and refinancing without increasing the total loan amount.

Worked Example

Sarah and Tom earn a combined $130,000 before tax. Sarah has a $5,000 student loan and Tom has a credit card with a $10,000 limit. They want to borrow $700,000 for a home.

Total debt: $700,000 + $5,000 + $10,000 = $715,000

DTI: $715,000 ÷ $130,000 = 5.5

Their DTI is under 6, so they would not be classified as high-DTI owner-occupier borrowers.

New builds are exempt from both LVR and DTI restrictions, making them a strong option for first home buyers who are constrained by either rule.

Low Equity Fees and Margins

If you purchase with less than a 20% deposit outside the First Home Loan scheme, most banks will charge you extra. This comes in two forms.

Low Equity Margin (LEM)

An additional interest rate margin added on top of the standard rate. The margin depends on the size of your deposit and typically ranges from 0.25% (with a 15% to 20% deposit) to 0.75% or more (with a 10% to 15% deposit). This margin stays in place until you reach 20% equity in your property, either through repayments or an increase in property value. You will need a registered valuation to prove your equity position when requesting removal.

Low Equity Premium (LEP)

A one-off upfront fee, usually around 0.75% of the loan amount, added to your mortgage balance. Unlike a LEM, this is not removed when you reach 20% equity because it has already been charged.

Each bank applies these differently. Some charge a LEM, some charge a LEP, and some offer a choice. The approach that works out cheaper depends on how quickly you expect to reach 20% equity.

Under the First Home Loan scheme, most participating lenders offer their standard or special interest rates without a low equity margin. The 1.2% lenders mortgage insurance fee replaces the bank’s own low equity charges, which in many cases makes the First Home Loan the cheaper option for eligible buyers.

Interest Rates

Your interest rate determines how much you pay the bank on top of the amount you borrow. Even a small difference in rate can add up to thousands of dollars over the life of your mortgage.

Fixed vs Floating Rates

Fixed rate: Your interest rate is locked in for a set period (usually one to five years). Your repayments stay the same for that period regardless of what happens in the wider market. At the end of the fixed term, you refix at the rates available at that time, or switch to a floating rate.

Floating rate: Your interest rate moves up and down in response to market conditions. Repayments can change at any time. Floating rates are typically higher than fixed rates but offer flexibility. You can make extra repayments or repay the loan in full without break fees.

Read our comparison on fixed vs floating rates to learn more.

How the OCR Affects Mortgage Rates

The Official Cash Rate (OCR) is set by the Reserve Bank of New Zealand and influences the cost of borrowing across the economy. When the RBNZ lowers the OCR, banks generally reduce their floating rates and shorter-term fixed rates. When the RBNZ raises the OCR, rates tend to rise.

As at March 2026, the OCR sits at 2.25% after nine consecutive cuts since August 2024. The RBNZ held the OCR at 2.25% at its February 2026 meeting. Most economists expect the OCR to remain stable through the first half of 2026, with potential increases toward the end of the year as the economy recovers.

Fixed mortgage rates are driven more by wholesale swap rates than the OCR. Swap rates are forward-looking, meaning they can move before the RBNZ makes a decision. This is why fixed rates sometimes rise even when the OCR has not changed.

Structuring Your Mortgage

Most mortgage brokers recommend splitting your loan across multiple fixed terms rather than locking everything into one rate. This strategy means a portion of your loan comes up for refixing at regular intervals, smoothing out the impact of rate changes over time. A common structure for a first home buyer is to split the loan into two or three portions fixed for one, two and three years.

Getting Pre-Approved

Pre-approval (also called conditional approval or approval in principle) is a written indication from a lender that they are willing to lend you a certain amount, subject to conditions. It is not a guarantee of finance, but it gives you a clear budget and signals to real estate agents that you are a serious buyer.

Why Pre-Approval Matters

- It sets a realistic price range so you don’t waste time looking at properties you cannot afford.

- It gives you confidence to make an offer when you find the right property.

- It is essential if you want to bid at auction, where offers are unconditional from the fall of the hammer.

- It speeds up the finance condition process once you have a signed sale and purchase agreement.

Documents You Will Need

- Photo ID (passport or NZ driver licence)

- Proof of income (payslips, employment contract, or two years of financial statements if self-employed)

- Bank statements for the past three months

- Details of existing debts and assets

- KiwiSaver balance statement (if using it toward your deposit)

- Gift declaration (if receiving a gifted deposit from family)

How Long Pre-Approval Takes

Pre-approval typically takes two to five working days from a complete application. It is usually valid for 60 to 90 days depending on the lender. If it expires before you find a property, you can apply to extend it.

Finding the Right Property

Where to Search

The main property listing platforms in New Zealand are:

For estimated property values and recent sales data, check homes.co.nz, OneRoof or QV. Be aware that the rateable value (RV) on a property is not the same as its market value. RVs are updated every three years and do not reflect renovations or market movements between updates.

Methods of Sale

Properties in New Zealand are sold through several methods. Each works differently, and understanding the process before you start making offers is important.

Advertised Price

The most common method. The property is listed with a price or price range and you make a written offer through a sale and purchase agreement. The seller can accept, reject or counter your offer.

Auction

You bid against other buyers on the day. If the hammer falls to you, the sale is unconditional immediately. You must have finance arranged and due diligence completed before the auction. A deposit (usually 10%) is payable on the day.

Deadline sale/tender

You submit a written offer by a set date. The seller reviews all offers after the deadline and chooses one (or none). Offers are confidential, so you do not know what others have offered.

Price by negotiation

No price is listed. You make an offer based on your research. This method can be frustrating for buyers who want a clear price guide.

Multi-Offer Situations

If more than one buyer makes an offer on the same property around the same time, the agent will inform all parties that a multi-offer situation exists. You will be given the opportunity to submit your best offer. This process is governed by the Real Estate Authority’s rules and the agent is required to treat all offers fairly.

Making an Offer

When you are ready to make an offer, you (or your lawyer) will prepare a sale and purchase agreement. This is a legally binding contract between you and the seller, so you should have your lawyer review it before you sign.

Common Conditions to Include

For a conditional offer (which is standard outside of auction), you should consider including the following conditions:

- Subject to finance: Gives you time to obtain formal loan approval from your lender. Without this condition, you are committed to the purchase even if your loan falls through.

- Subject to a satisfactory building report: Allows you to have the property inspected by a qualified building inspector and withdraw if major issues are found.

- Subject to a satisfactory LIM report: A Land Information Memorandum from the local council provides information about the property and land, including consents, drainage, hazards and any notices.

- Subject to solicitor’s approval: Gives your lawyer the right to review the agreement and the title and raise any issues before you are committed.

- Subject to valuation: Your lender may require an independent registered valuation, especially for low-deposit lending. This condition protects you if the valuation comes in lower than the purchase price.

Condition Timeframes

Standard condition timeframes are 10 to 15 working days. If you are using KiwiSaver and the First Home Loan scheme, you may need longer. KiwiSaver withdrawals and First Home Loan applications typically take 10 to 15 working days to process, and you need at least four weeks from application to settlement if you do not have pre-approval for the First Home Loan.

The Deposit

Once your offer is accepted and all conditions are satisfied (the agreement goes “unconditional”), and you pay a deposit into a trust account held by the real estate agency or your lawyer. The deposit is usually 5% to 10% of the purchase price but is negotiable. This deposit forms part of your total deposit and is held in trust until settlement.

Due Diligence

Due diligence is the process of checking everything about the property before you commit to buying it. This is your safety net. Cutting corners here to save money can lead to expensive surprises.

Building Report

A building inspection by a qualified inspector will identify structural issues, weathertightness problems, moisture damage, roofing and cladding condition, electrical and plumbing compliance and any other maintenance concerns. Expect to pay between $500 and $1,000 depending on the size and complexity of the property. This is money well spent. A good building inspector will flag major issues (like a roof that needs replacing within two years) that could cost tens of thousands of dollars.

LIM Report

A Land Information Memorandum (LIM) is issued by the local council and provides information including building consents and code compliance certificates (CCCs), drainage and sewerage, erosion or flood risk, any outstanding council notices, and whether the property is in a special zone (heritage, hazard, etc). LIM reports typically cost $200 to $400 and can take up to 10 working days to arrive.

Missing code compliance certificates (CCCs) can be a red flag. If building work was done without a CCC, it may affect your ability to get insurance and could impact your lender’s willingness to approve the loan.

Title Search

Your lawyer will conduct a title search to check for any encumbrances, easements, covenants or caveats on the property title. These can restrict what you can do with the property (for example, a covenant might prevent you from building a second dwelling). Your lawyer should explain any title issues in plain language before you go unconditional.

Registered Valuation

If you are buying with less than a 20% deposit, most banks will require a registered valuation by an independent, bank-approved valuer. This is separate from the council’s rateable value and from online estimates. Expect to pay between $850 and $1,500 depending on the property and valuer. If you need it urgently, add $200 or more for a rush fee. Your mortgage broker or lender can arrange this for you.

Going Unconditional

Once all conditions in the sale and purchase agreement have been satisfied (finance confirmed, building report satisfactory, LIM reviewed, solicitor’s approval given), you confirm to the seller’s agent or lawyer that you are going unconditional. At this point, both you and the seller are legally committed to completing the sale. The deposit is paid and held in trust until settlement.

Settlement Day

Settlement day is when ownership officially transfers to you. Your lawyer handles the legal side, including transferring funds, registering the property in your name and ensuring the mortgage is registered against the title.

What Happens on Settlement Day

- Your lawyer receives the loan funds from your lender.

- Your lawyer transfers the purchase price (minus the deposit already paid) to the seller’s lawyer.

- The seller’s lawyer confirms receipt and authorises the release of keys.

- The property title is transferred into your name.

- You collect the keys, usually from the real estate agent.

Before Settlement Day

- Arrange property insurance. Your lender may require proof of insurance before releasing funds.

- Do a pre-settlement inspection to confirm the property is in the same condition as when you made your offer and that all fixtures and chattels listed in the agreement are still there.

- Confirm your KiwiSaver funds have been released to your solicitor’s trust account.

- Arrange utilities (power, gas, internet, water) to be connected in your name from settlement day.

Costs Beyond the Deposit

Many first home buyers underestimate the additional costs of purchasing a property. Budget for these on top of your deposit.

| Cost | Estimated Range | Notes |

|---|---|---|

| Legal/conveyancing fees | $1,500 – $3,000+ | Fixed-fee conveyancing is available. Costs vary if complications arise (body corporate, cross-lease, etc.) |

| Registered valuation | $850 – $1,500 | Usually required for low-deposit lending. Your broker can arrange this. |

| Building inspection | $500 – $1,000 | Essential for older homes. More complex properties cost more. |

| LIM report | $200 – $400 | Ordered from the local council. Allow up to 10 working days. |

| LMI fee (First Home Loan) | 1.2% of loan amount | Can be added to the loan. On a $600,000 loan, this is $7,200. |

| Low equity fee/margin | 0.25% – 2.0% | Applies if buying with less than 20% outside the First Home Loan scheme. |

| Moving costs | $200 – $1,000+ | Within a city vs between cities. DIY vs professional movers. |

| Property insurance | $1,000 – $3,000+ per year | Required by your lender before settlement. Shop around or talk to insurance brokers. |

| Contents insurance | $300 – $800+ per year | Not required by your lender but highly recommended. |

| Rates | Varies by council | Payable quarterly or annually. Check the listing for the annual rates figure. |

Some lenders offer cash contributions toward legal fees as an incentive for new lending. Ask your mortgage broker whether any lender on the panel is offering cashback deals that could offset some of these costs.

Insurance

Property Insurance

Your lender will require you to have property insurance in place before they release mortgage funds on settlement day. Property insurance covers the cost of repairing or rebuilding the physical structure of your home if it is damaged by fire, storm, earthquake or other insured events. Make sure the sum insured reflects the full rebuild cost, not the market value or purchase price of the property.

Contents Insurance

Contents insurance covers your belongings inside the home. It is not a lender requirement, but it is strongly recommended. If your furniture, appliances or personal items are damaged or stolen, contents insurance covers the cost of replacement.

Life and Income Protection Insurance

A mortgage is a long-term financial commitment. If you or your partner become seriously ill, are injured, or pass away, life insurance and income protection can cover your mortgage repayments or pay off the loan entirely. This is not a lender requirement, but it is worth discussing with a financial adviser, especially if you have dependents or a single income household.

The Bright-Line Test

The bright-line test is a tax rule that applies when you sell a residential property within a set period of owning it. If the test applies, you may need to pay income tax on any gain from the sale.

Current Bright-Line Period

For properties acquired on or after 1 July 2024, the bright-line period is two years. If you sell within two years of acquisition and no exemption applies, tax is payable on the profit.

Main Home Exemption

If the property is your main home for at least 50% of the time you own it (measured by both time and floor area), the main home exemption applies and no bright-line tax is payable. As a first home buyer purchasing a property to live in, this exemption will almost always cover you. However, be aware that the exemption can only be used twice in a two-year period.

Even if the bright-line test does not apply, the IRD can still tax property gains if you purchased with an intention to sell at a profit. This is assessed under the general tax rules and is separate from the bright-line test.

Working With a Mortgage Broker

A mortgage broker (also called a mortgage adviser) works on your behalf to find the right home loan for your situation. Unlike a bank, a broker has access to multiple lenders and can compare options across the market.

What a Broker Does for First Home Buyers

- Assesses your financial position and advises how much you can realistically borrow.

- Identifies which government schemes (First Home Loan, KiwiSaver withdrawal) you qualify for.

- Compares rates, fees and lending criteria across their lender panel.

- Prepares and submits your loan application.

- Manages the process from pre-approval through to settlement.

- Recommends a mortgage structure (how to split your loan across fixed terms).

How Brokers Are Paid

For standard home loans, mortgage brokers are paid a commission by the lender when your loan settles. This means there is usually no cost to you. The commission does not affect your interest rate. In some complex or short-term lending situations, a broker fee may apply, but this will always be discussed with you upfront.

Choosing a Broker

Make sure your broker is a licensed financial adviser operating under a Financial Advice Provider (FAP) licence regulated by the Financial Markets Authority (FMA). Check their registration on the Financial Service Providers Register (FSPR). They should provide you with a disclosure statement before giving you advice.

Common Mistakes First Home Buyers Make

- Not getting pre-approved before house hunting. Without pre-approval, you risk falling in love with a property you cannot afford, or losing out to a buyer who is ready to move.

- Forgetting to budget for costs beyond the deposit. Legal fees, valuations, inspections, insurance and moving costs can easily add $5,000 to $15,000 on top of your deposit.

- Skipping the building inspection. A $700 building report is cheap compared to discovering a $40,000 roof replacement after you have moved in.

- Not closing unused credit facilities. Banks count credit card limits against your DTI even if you owe nothing. A $20,000 credit card you never use could reduce your borrowing capacity by $100,000 or more.

- Rushing to go unconditional. Take the full condition period to complete your due diligence. Once you go unconditional, you are legally committed.

- Not seeking independent legal advice. The real estate agent works for the seller, not for you. Your lawyer or conveyancer is the person looking out for your interests.

- Assuming the rateable value is the market value. RVs can be significantly higher or lower than what a property would sell for. Use actual comparable sales data and a registered valuation instead.

- Waiting too long to start your KiwiSaver application. Allow at least 10 to 15 working days for the withdrawal to process. If you leave it too late, you could miss your deadline.

Frequently Asked Questions

Who qualifies as a first time home buyer in New Zealand?

In New Zealand, you’re generally considered a first time home buyer if you have never owned residential property or land before. This applies whether you’re purchasing alone or with a partner. You do not need to be a certain age, and there is no set timeframe for how long you’ve been renting or saving.

How much can a first home buyer borrow?

How much you can borrow as a first home buyer depends on your gross income, existing debts and financial commitments, the interest rate used by the lender to assess affordability, and your deposit amount. Talk to our mortgage brokers for a personalised assessment.

Can I rent out my first home?

If you used a standard owner-occupier home loan with a 20% deposit, your lender will generally expect you to live in the property initially, but most will allow you to rent it out later. If you purchased using a Kāinga Ora First Home Loan, you cannot rent the property out while you’re on that scheme. The loan requires you to live in the home as your primary residence. If your circumstances change and you wish to rent the property, you would need to refinance to a standard mortgage first. Our team can help you work through the refinancing process when the time is right.

Is the First Home Grant still available?

No. The Kainga Ora First Home Grant was discontinued on 22 May 2024. However, the First Home Loan (5% deposit scheme) and the KiwiSaver first home withdrawal are both still available.

What is the difference between LVR and DTI?

LVR (loan-to-value ratio) limits how much you can borrow relative to the property value. It determines the deposit you need. DTI (debt-to-income) limits how much total debt you can have relative to your income. Both restrictions apply simultaneously. You need to satisfy both to get a standard bank home loan.

How long does the home buying process take?

From pre-approval to settlement, the process typically takes two to four months depending on how quickly you find a property. Pre-approval takes two to five working days. Once you have a signed sale and purchase agreement, the condition period is usually 10 to 15 working days. Settlement is agreed between buyer and seller but is commonly four to six weeks after going unconditional.

Can I buy my first home if I’m self-employed?

Yes. Self-employed borrowers can get home loans, though lenders typically require two years of financial statements (tax returns and financial accounts) to verify income. Some lenders are more flexible than others. A mortgage broker who understands self-employed lending can match you with the right lender for your situation.

What happens if my property valuation comes in lower than the purchase price?

If the registered valuation is lower than the price you have agreed to pay, your lender may reduce the amount they are willing to lend. You will either need to make up the difference with additional deposit funds, renegotiate the purchase price with the seller, or withdraw from the agreement (if you have a valuation condition in your sale and purchase agreement).

Do I pay tax when I sell my first home?

If the property is your main home and you have lived in it for at least 50% of the time you owned it, the main home exemption applies to the bright-line test and no tax is payable on any gain from the sale. If you sell within two years and the exemption does not apply, income tax is payable on the profit at your marginal tax rate.

Should I fix my mortgage rate or go floating?

Most New Zealand borrowers fix their mortgage rate. As at March 2026, short-term fixed rates (one to two years) are generally lower than floating rates and offer certainty of repayments. Many borrowers split their loan across multiple terms to balance certainty with flexibility. A mortgage broker can help you decide on a structure based on your circumstances and the current rate outlook.

How much does a mortgage broker cost?

For standard home loans, our service is free. Lenders pay us a commission when your loan settles, which does not affect your interest rate. For some specialist or short-term lending, a broker fee may apply. We always discuss this with you before proceeding.

Ready to Take the Next Step?

Buying your first home is a big milestone, and having the right support makes all the difference. At OneStop Financial Solutions, we help first home buyers across New Zealand with mortgage advice, access to government schemes and a clear plan from your first conversation through to settlement day.

Whether you are just starting to save, ready for pre-approval, or actively looking at properties, we are here to help you work through your options.

Book a free consultation:

Phone: 021 022 17130

Email: service@onestopfs.co.nz or complete our form below

Office: Level 2/26 Aviemore Drive, Highland Park, Auckland 2010

Online consultations available nationwide.

Disclaimer: The information on this page is general in nature and does not take into account your individual financial situation or goals. Before making any financial decisions, you should consider whether the products and services mentioned are appropriate for your circumstances. A disclosure statement is available on request and free of charge.